In the realm of banking, US ABA numbers serve as a cornerstone for ensuring seamless transactions and precise processing of financial activities. Officially known as American Bankers Association (ABA) routing numbers, these unique nine-digit codes are assigned exclusively to financial institutions within the United States. Gaining a clear understanding of how ABA numbers function is crucial for anyone involved in domestic or international banking operations.

ABA numbers are far from arbitrary sequences of digits; they encode specific details that help identify the financial institution and facilitate the smooth movement of funds. Whether you're configuring direct deposits, transferring funds between accounts, or handling online bill payments, knowing how to locate and utilize your ABA number is essential for ensuring that your transactions are processed accurately and efficiently.

As we progress through this article, you'll acquire a thorough understanding of US ABA numbers, including their structure, purpose, and functionality within the banking ecosystem. By the conclusion of this guide, you'll appreciate why ABA numbers are indispensable in the contemporary financial landscape.

Read also:Discover The Best With L Eagle Services Your Ultimate Guide

Table of Contents

- What is an ABA Number?

- Structure of an ABA Number

- Importance of ABA Numbers

- How to Find Your ABA Number

- ABA Number vs. SWIFT Code

- Common Uses of ABA Numbers

- History of ABA Numbers

- Security and Privacy Concerns

- Challenges with ABA Numbers

- The Future of ABA Numbers

What is an ABA Number?

An ABA number, also referred to as a routing transit number (RTN), is a nine-digit code utilized in the United States to distinguish financial institutions. Initially introduced in 1910 by the American Bankers Association to streamline the processing of paper checks, its application has since expanded to encompass electronic funds transfers, direct deposits, and other financial operations.

Key Features of ABA Numbers

ABA numbers are uniquely assigned to each financial institution, providing essential data for payment processing. Below are some of their defining characteristics:

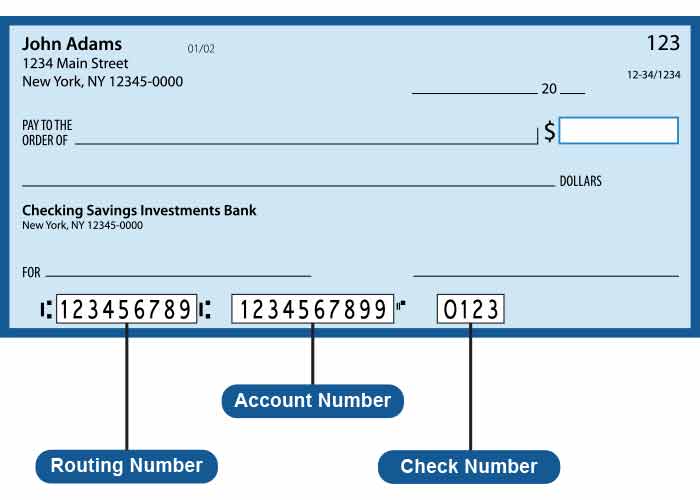

- Identifies the Bank: The initial four digits of the ABA number specify the Federal Reserve district where the bank is situated.

- Bank Branch: The subsequent four digits pinpoint the specific bank branch within the district.

- Checksum Digit: The final digit functions as a checksum to confirm the accuracy of the ABA number.

ABA numbers are pivotal for domestic transactions in the U.S., guaranteeing that funds are routed correctly and expeditiously.

Structure of an ABA Number

The structure of an ABA number is meticulously crafted to encode precise information about the financial institution. Each of the nine digits in the code serves a distinct purpose, facilitating the identification of the bank and validation of the number.

Breaking Down the ABA Number

Here's a detailed breakdown of the ABA number's structure:

- Digits 1-4: These digits denote the Federal Reserve routing symbol, correlating to the bank's geographic location.

- Digits 5-8: These digits represent the bank's unique identifier, differentiating it from other institutions within the same district.

- Digit 9: This digit acts as the checksum, ensuring the ABA number's validity.

Grasping the structure of an ABA number is instrumental in ensuring that financial transactions are processed without errors.

Read also:Discovering The Timeless Talent Of Billy Crystal A Closer Look At His Age And Achievements

Importance of ABA Numbers

ABA numbers are indispensable in the banking sector, serving as the backbone of domestic transactions in the United States. Their significance transcends merely identifying financial institutions, as they play a critical role in preserving the integrity and efficiency of the banking system.

Why ABA Numbers Matter

- Accuracy: ABA numbers ensure that funds are routed to the appropriate bank and account, minimizing errors in financial transactions.

- Security: The checksum digit aids in fraud prevention by verifying the validity of the ABA number.

- Efficiency: ABA numbers enhance the processing of checks, electronic transfers, and other financial activities, reducing delays and processing times.

In the absence of ABA numbers, the banking system would encounter substantial difficulties in processing transactions accurately and efficiently.

How to Find Your ABA Number

Locating your ABA number is a straightforward process, with several methods available depending on your requirements. Whether you're setting up direct deposits or executing fund transfers, knowing how to find your ABA number is crucial for completing transactions.

Methods to Locate Your ABA Number

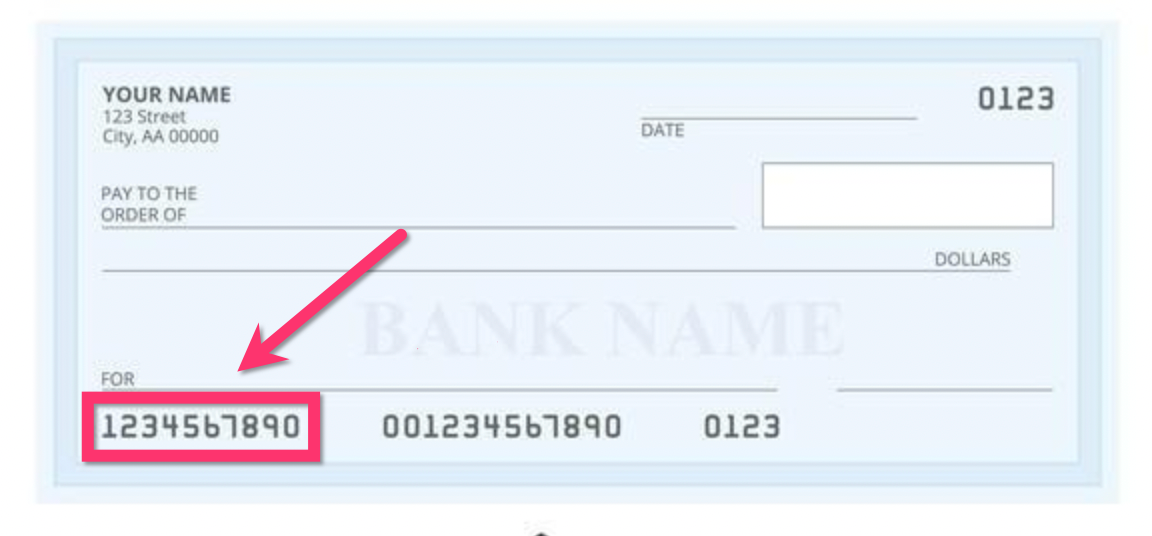

- Check Your Checks: The ABA number is usually printed on the bottom-left corner of your checks.

- Online Banking: Most banks display the ABA number in the account details section of their online banking platforms.

- Customer Service: If you're uncertain about locating your ABA number, you can reach out to your bank's customer service for assistance.

It's essential to verify the ABA number with your bank to ensure its accuracy, especially when handling sensitive financial transactions.

ABA Number vs. SWIFT Code

While ABA numbers cater to domestic transactions within the United States, SWIFT codes are employed for international transfers. Understanding the distinctions between these systems is vital for anyone involved in global banking activities.

Key Differences

- Purpose: ABA numbers are tailored for domestic transactions, whereas SWIFT codes are utilized for international transfers.

- Structure: ABA numbers consist of nine digits, while SWIFT codes are alphanumeric and range from eight to eleven characters in length.

- Scope: ABA numbers are exclusive to the U.S., whereas SWIFT codes are utilized globally across various financial institutions.

Selecting the appropriate code for your transaction, whether domestic or international, ensures that funds are processed correctly.

Common Uses of ABA Numbers

ABA numbers find application in numerous aspects of the banking industry, making them an essential component of financial transactions. Below are some of the most prevalent uses:

Applications of ABA Numbers

- Direct Deposits: Employers leverage ABA numbers to deposit salaries directly into employees' bank accounts.

- Bill Payments: ABA numbers are necessary for setting up automatic bill payments and transfers.

- Wire Transfers: Domestic wire transfers depend on ABA numbers to ensure funds are sent to the correct recipient.

These applications underscore the versatility and importance of ABA numbers in facilitating everyday financial activities.

History of ABA Numbers

The origins of ABA numbers date back to 1910 when the American Bankers Association introduced them to standardize check processing. Over the decades, ABA numbers have evolved to accommodate the increasing complexity of the banking industry, adapting to new technologies and transaction methods.

Evolution of ABA Numbers

Initially designed for paper checks, ABA numbers have expanded their role to include electronic funds transfers and other digital transactions. This evolution demonstrates the banking industry's dedication to innovation and efficiency, ensuring that ABA numbers remain relevant in today's dynamic financial environment.

Security and Privacy Concerns

Like any financial information, ABA numbers necessitate careful handling to protect against fraud and unauthorized access. While ABA numbers are generally secure for domestic transactions, it's crucial to exercise caution when sharing them with third parties.

Best Practices for Security

- Limit Sharing: Share your ABA number exclusively with trusted entities, such as employers or financial institutions.

- Monitor Transactions: Regularly review your bank statements to identify any suspicious activity.

- Use Secure Channels: When transmitting ABA numbers electronically, ensure the use of secure platforms and encryption methods.

By adhering to these best practices, you can safeguard your ABA number and protect your financial information from potential threats.

Challenges with ABA Numbers

Despite their significance, ABA numbers are not devoid of challenges. Issues such as outdated systems, fraud risks, and the need for modernization pose potential obstacles in the banking industry.

Addressing Challenges

- System Updates: Financial institutions must continuously update their systems to accommodate new technologies and transaction methods.

- Fraud Prevention: Implementing robust security measures is essential for safeguarding ABA numbers from fraudulent activities.

- Modernization: As digital banking continues to advance, there is a growing need to adapt ABA numbers to meet the demands of modern financial systems.

Overcoming these challenges requires collaboration between banks, regulators, and technology providers to ensure that ABA numbers remain effective and secure.

The Future of ABA Numbers

As the banking industry continues to progress, the future of ABA numbers appears promising. Advancements in technology and the increasing adoption of digital banking solutions are driving innovations in how ABA numbers are utilized and managed.

Trends and Innovations

- Digital Integration: ABA numbers are becoming increasingly integrated into digital platforms, enhancing their usability and accessibility.

- Blockchain Technology: Emerging technologies like blockchain could transform how ABA numbers are used, offering enhanced security and transparency.

- Global Expansion: While predominantly used in the U.S., there is potential for ABA numbers to expand their role in international transactions, bridging the gap between domestic and global banking systems.

The future of ABA numbers holds exciting possibilities, ensuring that they remain a vital component of the financial landscape for years to come.

Conclusion

In summary, US ABA numbers are an integral part of the banking system, facilitating accurate and efficient financial transactions. From their inception in 1910 to their current role in digital banking, ABA numbers have proven to be indispensable tools for domestic transactions. Understanding their structure, importance, and applications is crucial for anyone involved in banking activities.

We encourage you to share this article with others who may benefit from learning about ABA numbers. If you have any questions or insights, feel free to leave a comment below. Additionally, explore our other articles for more valuable information on financial topics. Together, let's continue to expand our knowledge and enhance our financial literacy.