ABA numbers and routing numbers are terms frequently used interchangeably, but do they truly mean the same thing? If you're unsure about whether an ABA number is the same as a routing number, you're not alone. Gaining a clear understanding of these financial terms is essential for effectively managing your bank accounts and transactions.

In the world of banking, terms like ABA numbers and routing numbers may seem complex and confusing. However, understanding these concepts can significantly enhance your financial literacy. These numbers play a crucial role in ensuring the secure movement of funds between accounts, making them indispensable in today’s financial landscape.

This article will delve into the world of ABA numbers and routing numbers, exploring their similarities, differences, and importance. Whether you're setting up direct deposits, initiating wire transfers, or simply trying to understand your bank statements, this guide will provide you with the clarity you need to manage your finances confidently.

Read also:Unleashing The Power Of Shelby Rush Energy Your Ultimate Guide

Table of Contents

- Overview of ABA Numbers

- What Exactly is a Routing Number?

- Are ABA Numbers and Routing Numbers the Same?

- How to Locate Your ABA Number

- Common Uses of ABA Numbers

- The History of ABA Numbers

- What Do the Digits in an ABA Number Represent?

- ABA Number Security Best Practices

- Frequently Asked Questions About ABA Numbers

- Conclusion: Why Understanding ABA Numbers is Essential

Overview of ABA Numbers

An ABA number, also known as the American Bankers Association number, is a nine-digit code assigned to financial institutions in the United States. This unique identifier ensures that funds are routed correctly between banks and credit unions, facilitating secure domestic transfers, direct deposits, and other financial activities.

Why Are ABA Numbers Important?

ABA numbers are fundamental to the smooth functioning of the banking system, enabling accurate and secure transactions. Below are some key reasons why ABA numbers are indispensable:

- They ensure that funds are accurately routed between financial institutions.

- They help prevent fraud by verifying the legitimacy of financial institutions.

- They streamline processes such as direct deposits, bill payments, and wire transfers.

As reported by the Federal Reserve, millions of transactions are processed daily using ABA numbers, making them a cornerstone of the U.S. financial infrastructure.

What Exactly is a Routing Number?

A routing number, also referred to as a routing transit number (RTN), is a nine-digit code utilized by banks and financial institutions in the United States. Its primary role is to identify the specific bank or credit union involved in a transaction. Routing numbers are critical for processing checks, initiating wire transfers, and setting up direct deposits.

How Routing Numbers Function

Routing numbers act as a digital address for banks, ensuring that funds are directed to the correct institution. For instance, when depositing a check, the routing number on the check helps the bank verify the origin of the funds and credit the appropriate account. Similarly, during electronic transfers, routing numbers guide the movement of money from one account to another.

The American Bankers Association first introduced routing numbers in 1910 to standardize banking operations across the country. Today, they remain a vital component of the U.S. financial system.

Read also:Discover The Ultimate Relaxation At Flirt Spa And Brow Bar

Are ABA Numbers and Routing Numbers the Same?

Yes, an ABA number is the same as a routing number. Both terms refer to the nine-digit code assigned to financial institutions in the United States. While the terminology may differ—“ABA number” being more formal and “routing number” more commonly used in everyday language—their function remains consistent. They ensure accurate and secure financial transactions.

Key Similarities Between ABA and Routing Numbers

- Both consist of nine digits.

- Both serve as identifiers for banks and credit unions.

- Both are used to route funds during transactions.

Whether referred to as an ABA number or a routing number, the underlying purpose is the same: to facilitate precise and secure financial transactions.

How to Locate Your ABA Number

Finding your ABA number is a simple process. Below are some common methods to help you locate it:

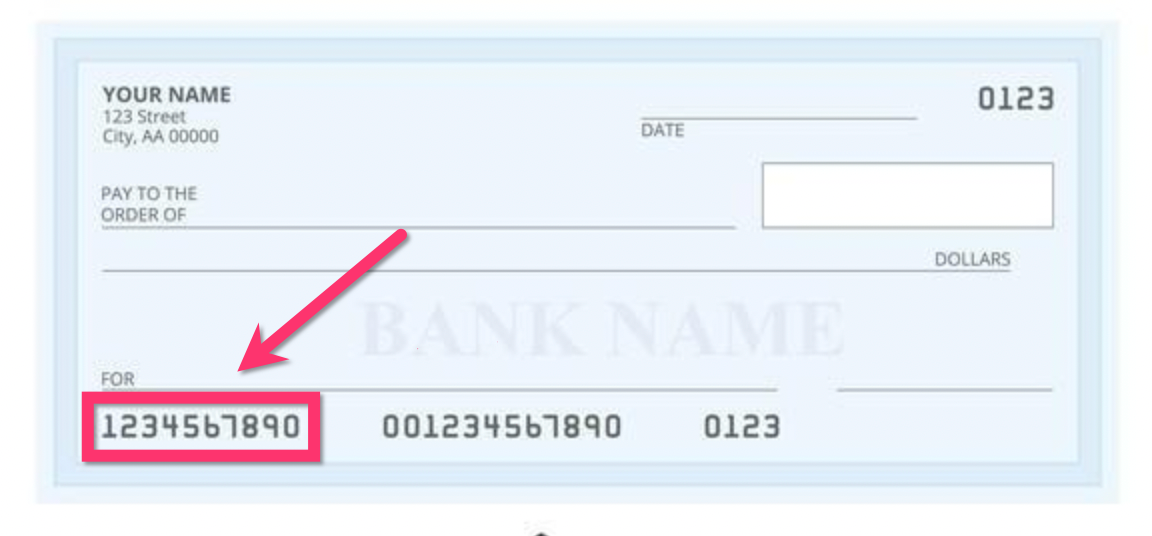

1. Check Your Personal Checks

One of the easiest ways to find your ABA number is by examining the bottom of your personal checks. The nine-digit code located on the left side of the check is your ABA number.

2. Use Online Banking

Most banks provide your routing number through their online banking platforms. Log in to your account, navigate to the account information section, and you should find your ABA number listed there.

3. Contact Your Bank

If you're unable to locate your ABA number through checks or online banking, you can contact your bank's customer service department. They will be able to provide you with the correct routing number for your account.

Common Uses of ABA Numbers

ABA numbers are utilized in a variety of financial transactions. Below are some of the most common uses:

1. Direct Deposits

When setting up direct deposits for your paycheck or government benefits, you'll need to provide your ABA number to ensure the funds are deposited into the correct account.

2. Wire Transfers

ABA numbers are essential for domestic wire transfers. They help banks verify the sending and receiving accounts, ensuring the funds are transferred accurately.

3. Bill Payments

Many bill payment services require your ABA number to process payments automatically from your bank account. This ensures timely payments without the need for manual intervention.

The History of ABA Numbers

The origins of ABA numbers date back to 1910 when the American Bankers Association introduced them to standardize banking operations. At the time, the U.S. banking system was fragmented, with no uniform method for identifying financial institutions. The creation of ABA numbers revolutionized the industry by providing a consistent and reliable way to route transactions.

Over the years, ABA numbers have evolved to accommodate technological advancements and changes in the financial landscape. Today, they remain a critical component of the U.S. banking infrastructure, supporting millions of transactions daily.

What Do the Digits in an ABA Number Represent?

Each digit in an ABA number has a specific meaning. Understanding the structure of these numbers can provide insight into how they function:

1. First Four Digits

The first four digits represent the Federal Reserve routing symbol. This identifies the Federal Reserve Bank responsible for processing transactions involving the financial institution.

2. Next Four Digits

The next four digits are the bank identifier. They uniquely identify the specific financial institution associated with the ABA number.

3. Last Digit

The final digit is a check digit used to verify the accuracy of the ABA number. It is calculated using a mathematical formula to ensure the number is valid.

This structure ensures that ABA numbers are both unique and verifiable, minimizing the risk of errors during transactions.

ABA Number Security Best Practices

While ABA numbers are essential for banking operations, they also pose potential security risks if misused. Below are some tips to help protect your ABA number:

1. Keep It Confidential

Avoid sharing your ABA number unnecessarily. Only provide it to trusted entities, such as your employer for direct deposits or your bank for wire transfers.

2. Monitor Your Accounts

Regularly review your bank statements for any unauthorized transactions. If you suspect fraud, contact your bank immediately to report the issue.

3. Use Secure Channels

When transmitting your ABA number electronically, ensure you're using secure channels, such as encrypted email or secure online banking platforms.

Frequently Asked Questions About ABA Numbers

1. Can I Use the Same ABA Number for Different Accounts?

In most cases, the ABA number is the same for all accounts within a single financial institution. However, some banks may issue different ABA numbers for specific types of accounts, such as business accounts or international transfers.

2. Are ABA Numbers Unique to Each Bank?

Yes, ABA numbers are unique to each financial institution. No two banks or credit unions will have the same ABA number.

3. Can I Find My ABA Number Without Checks?

Yes, you can find your ABA number through online banking or by contacting your bank's customer service department. Many banks also list ABA numbers on their websites for convenience.

Conclusion: Why Understanding ABA Numbers is Essential

Understanding whether an ABA number is the same as a routing number is crucial for effectively managing your finances. These nine-digit codes play a vital role in ensuring accurate and secure transactions, from direct deposits to wire transfers. By familiarizing yourself with ABA numbers and their functions, you can navigate the banking system with confidence.

We encourage you to take the following steps:

- Locate your ABA number and verify its accuracy.

- Use secure channels when sharing your ABA number.

- Stay informed about the latest developments in banking security.

Share this article with friends and family to help them understand the importance of ABA numbers. For more insights into personal finance and banking, explore our other articles on the website.