Are you puzzled about whether an ABA number and a routing number are the same? You're not alone. Many individuals find these terms confusing, especially when navigating banking transactions. Gaining clarity on the relationship between ABA numbers and routing numbers is crucial for effectively managing your finances.

In today's digital era, where online banking and financial transactions are increasingly common, having a solid understanding of banking terminology is essential. This article will provide an in-depth exploration of ABA numbers, routing numbers, and their interconnectedness. By the end of this guide, you'll have a comprehensive understanding of these concepts and how they influence your financial activities.

Whether you're initiating money transfers, setting up direct deposits, or handling online bill payments, knowing the distinction between ABA numbers and routing numbers can save you time and reduce frustration. Let's delve into the details and demystify these critical banking codes.

Read also:Unveiling The World Of Game Fate Go A Journey Into Strategy And Adventure

Contents Overview

- What Exactly is an ABA Number?

- Comprehending Routing Numbers

- Are ABA Numbers and Routing Numbers Identical?

- The Evolution of ABA and Routing Numbers

Purpose of ABA and Routing Numbers

- Locating Your ABA/Routing Number

Key Distinctions Between ABA and Routing Numbers

- Security Concerns Regarding ABA/Routing Numbers

- Best Practices for Protecting Your ABA/Routing Number

- Final Thoughts

What Exactly is an ABA Number?

An ABA number, officially known as the American Bankers Association number, is a unique nine-digit code assigned to financial institutions in the United States. Introduced in 1910 by the American Bankers Association, its primary goal was to standardize bank identification and streamline check processing. Today, ABA numbers play a pivotal role in various banking operations, including wire transfers, direct deposits, and automated clearing house (ACH) transactions.

The core purpose of an ABA number is to ensure that financial transactions are accurately directed to the appropriate bank or credit union. Each bank or credit union is assigned a distinct ABA number, which minimizes errors and facilitates the seamless movement of funds between institutions. Understanding how ABA numbers function is indispensable for anyone involved in banking activities, particularly those involving electronic transfers.

Comprehending Routing Numbers

A routing number essentially serves the same function as an ABA number. It identifies financial institutions and ensures transactions are routed correctly to the intended bank or credit union. However, the term "routing number" has become more prevalent in modern banking, especially in digital contexts.

Routing numbers are crucial for processing checks, initiating wire transfers, and setting up direct deposits. They act as a digital address for banks, ensuring funds are directed to the right destination. Without a valid routing number, financial transactions cannot be successfully completed. This makes routing numbers a fundamental component of the banking system.

Are ABA Numbers and Routing Numbers Identical?

To put it simply, yes, an ABA number and a routing number are the same. Both terms refer to the nine-digit code used to identify banks and credit unions in the United States. While "ABA number" is the original term, "routing number" has gained popularity in recent years due to its broader application in electronic banking.

It's worth noting that while the terms are interchangeable, the context in which they are used may differ. For instance, ABA number is often used in check processing scenarios, whereas routing number is more commonly associated with electronic transactions. Regardless of the terminology, their primary function remains consistent: ensuring precise and efficient financial transactions.

Read also:Alex Morgan Age And Career Highlights Discover The Inspiring Journey Of A Soccer Legend

The Evolution of ABA and Routing Numbers

The origins of ABA and routing numbers trace back to the early 20th century when the American Bankers Association sought to enhance banking efficiency. In 1910, the ABA introduced the ABA number system to standardize the identification of financial institutions and simplify check processing. This innovation transformed the banking industry and paved the way for modern financial transactions.

Over time, the ABA number system adapted to technological advancements and evolving banking practices. The advent of electronic banking in the late 20th century further expanded the role of routing numbers, making them essential for a wide array of financial activities. Today, routing numbers are a cornerstone of the global financial system, facilitating billions of transactions annually.

Purpose of ABA and Routing Numbers

Domestic Financial Transactions

ABA and routing numbers are primarily utilized for domestic transactions within the United States. They enable banks and credit unions to efficiently process checks, wire transfers, and ACH transactions. Whether you're depositing a paycheck, paying bills online, or transferring funds to a friend, a valid routing number is essential for ensuring the successful completion of the transaction.

- Check processing

- Direct deposits

- Wire transfers

- ACH transactions

International Financial Transactions

While ABA and routing numbers are predominantly used for domestic transactions, they also play a role in international banking activities. For example, when transferring funds from a U.S.-based bank to an international account, a routing number is often required as part of the transaction details. However, additional identifiers, such as a SWIFT code, may be necessary for cross-border transactions.

It's important to recognize that routing numbers alone are insufficient for international transactions. Banks typically require additional information, such as IBAN or BIC codes, to ensure the accurate routing of funds across borders. Understanding the requirements for international transactions is vital for anyone engaged in global financial activities.

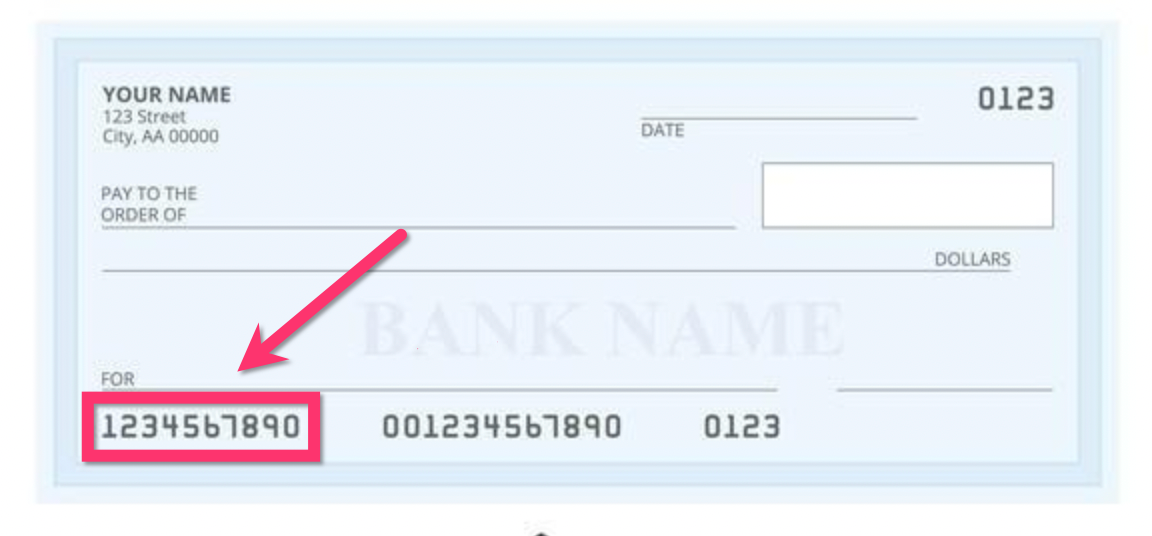

Locating Your ABA/Routing Number

Finding your ABA or routing number is straightforward and can be accomplished in several ways:

- Check the bottom of your personal checks: The routing number is usually the first set of numbers printed at the bottom left corner of the check.

- Online banking: Most banks display your routing number in the account information section of their online banking platforms.

- Bank website: Many banks publish their routing numbers on their official websites for easy access.

- Customer service: If you're unable to locate your routing number, you can contact your bank's customer service department for assistance.

Regardless of the method you choose, it's crucial to verify the accuracy of the routing number before using it for any financial transaction. Incorrect routing numbers can lead to delayed or failed transactions, so double-checking is always advisable.

Key Distinctions Between ABA and Routing Numbers

Formatting Differences

Although ABA and routing numbers are fundamentally the same, there may be slight variations in their format depending on the context in which they are used. For example:

- ABA numbers are typically used in check processing and may include additional characters or symbols for clarity.

- Routing numbers are more commonly used in electronic transactions and may be formatted differently to accommodate digital systems.

Despite these minor differences, both codes consist of nine digits and serve the same fundamental purpose of identifying financial institutions.

Usage Variations

The usage of ABA and routing numbers may vary slightly based on the type of transaction being conducted. For instance:

- ABA numbers are often used for check processing and manual transactions.

- Routing numbers are predominantly used for electronic transactions, such as wire transfers and ACH payments.

Understanding these nuances can help you choose the appropriate term based on the context of your banking activity.

Security Concerns Regarding ABA/Routing Numbers

While ABA and routing numbers are essential for banking transactions, they also pose certain security risks if mishandled. Sharing your routing number with unauthorized parties can potentially lead to fraudulent activities, such as unauthorized transfers or identity theft. It's crucial to safeguard your routing number and only provide it to trusted entities when necessary.

Most banks implement robust security measures to protect routing numbers and prevent unauthorized access. However, it's equally important for individuals to exercise caution when sharing sensitive financial information. By adopting best practices for securing your routing number, you can minimize the risk of fraud and ensure the safety of your financial transactions.

Best Practices for Protecting Your ABA/Routing Number

To safeguard your ABA/routing number and prevent potential fraud, consider the following tips:

- Only share your routing number with trusted financial institutions or service providers.

- Use secure methods of communication, such as encrypted email or secure messaging platforms, when sharing sensitive financial information.

- Regularly monitor your bank statements for any unauthorized transactions and report suspicious activity immediately.

- Enable two-factor authentication on your online banking accounts to add an extra layer of security.

- Stay informed about the latest security threats and best practices for protecting your financial information.

By following these tips, you can enhance the security of your ABA/routing number and protect yourself from potential financial fraud.

Final Thoughts

In summary, the terms ABA number and routing number are interchangeable and refer to the same nine-digit code used to identify financial institutions in the United States. Understanding the function and significance of these numbers is vital for anyone involved in banking activities, particularly those involving electronic transactions.

By familiarizing yourself with the history, purpose, and security considerations associated with ABA/routing numbers, you can make informed decisions about your financial transactions. Remember to safeguard your routing number and only share it with trusted entities to minimize the risk of fraud.

We encourage you to leave a comment or share this article with others who may benefit from this information. For more insightful content on personal finance and banking, explore our other articles on the website. Stay informed, stay secure, and take control of your financial future!